By: Hamna Shakeel

An economic corridor built on code and capital is quietly formalizing across the Arabian Sea. Following the enactment of the landmark Virtual Assets Act of 2026, the State Bank of Pakistan (SBP) issued BPRD Circular Letter No. 10 of the same year, which would dismantle an eight-year blanket prohibition on digital asset banking – fundamentally re-engineering the pipeline connecting Pakistan’s high-density software engineering pools with the institutional capital engines of the Gulf Cooperation Council (GCC).

For nearly a decade, the financial pipeline between Karachi, Dubai, and Riyadh operated under severe structural friction. While Pakistani developers built core infrastructure for global distributed ledger technology (DLT) projects, their earnings were largely obscured within the peer-to-peer (P2P) gray market or routed through cumbersome corporate proxies in the Gulf.

This new framework establishes a legal bridge, superseding the long-standing restrictions originally enforced under the State Bank of Pakistan’s BPRD Circular No. 03 of 2018 and officially ending the nation’s eight-year isolation from the traditional banking system.

It furthermore authorizes commercial lenders to open dedicated, non-interest-bearing Client Money Accounts (CMAs) denominated in Pakistani Rupees (PKR), specifically designed to custody fiat funds for licensed Virtual Asset Service Providers (VASPs) under strict anti-money laundering frameworks.

The Macroeconomic Symmetry

The emerging pipeline highlights a deep regional symbiosis: while the GCC provides the institutional scaffolding and capital, Pakistan serves as the technical engine room.

Where cities like Dubai and Riyadh – through the Virtual Assets Regulatory Authority (VARA) and the Saudi Central Bank (SAMA), respectively – have established sophisticated regulatory playgrounds, both face steep financial overheads when scaling localized, on-site engineering operations. By establishing clear regulatory guardrails under the Pakistan Virtual Assets Regulatory Authority (PVARA), the country has effectively institutionalized its cost-arbitrage talent pool.

Traditional lenders are strictly barred from direct digital asset exposure or trading via house capital. Instead, their role is restricted to providing transactional payment interfaces through dedicated, non-remunerative PKR Client Money Accounts. This strict segregation ring-fences user rupees from the VASP’s own operating capital, satisfying international anti-money laundering protocols and Financial Action Task Force (FATF) compliance standards.

Nevertheless, Syed Osama Zaidi, specialist in investment banking and TMT M&A, observes that the operational efficacy of these CMAs addresses only a fraction of the broader structural challenge:

“The Client Money Account framework has essentially streamlined a single vertical: localized settlement for licensed VASPs,” Zaidi explained to Fintech News Media.

“Financial institutions are now mandated to maintain distinct, ring-fenced PKR accounts to custody VASP transactional funds, ensuring total segregation from operating capital,” he said, adding that although this provides on-ground utility, it fails to resolve the primary anxieties of a Gulf-based institutional investor – especially in the form of friction surrounding capital repatriation, exit velocity, and robust bilateral investment treaties.

Consequently, the pipeline is evolving into a sophisticated hybrid architecture rather than a complete onshore migration. GCC capital is increasingly deployed to fuel Pakistani operational entities, financing technical hubs and PVARA-regulated subsidiaries, while the parent holding structures remain domiciled in Dubai or Abu Dhabi.

The “flip structure” has matured from a desperate legal improvisation into a formalized strategic standard: investors acknowledge the legitimacy of regulated Pakistani revenue streams, but remain steadfast in requiring that intellectual property, cap tables, and liquidity events be governed by the legal frameworks of the Gulf.

This bifurcation is dictated by stark macroeconomic variables. Institutional entities in Riyadh are deploying multi-year capital against a backdrop of currency volatility and rigorous IMF-mandated fiscal reforms. And while local regulatory clarity has rendered Pakistani technical teams bankable, it has not neutralized the underlying country risk.

As a result, direct onshore investment is largely confined to boutique checks from the diaspora, whereas the significant institutional liquidity continues to be channeled through established Gulf gateways.

The Founders’ Perspective

For fintech platforms operating across these borders, the legislative shift transforms day-to-day treasury operations from an ongoing compliance hurdle into a streamlined asset. Major global exchanges like Binance and HTX, in fact, have already initiated the local licensing pipeline, marking a shift toward institutional cross-border corridors.

“Before the 2026 Act, managing payroll and operational expenses for a dev shop of over 70 engineers in Karachi out of a Dubai holding entity required constant legal maneuvering,” noted a dual-region founder building enterprise liquidity rails between the UAE and Pakistan, who asked to remain anonymous.

“By legalizing client money accounts locally, we can finally stop treating our engineering base as an unanchored freelance network and start treating it as a formalized corporate asset. Gulf-based venture funds are already responding; we are seeing institutional investors actively mandate that portfolio companies base their technical back-ends in Karachi now that the legal shield is live,” they added.

The convergence of regulatory frameworks is also accelerating cross-border B2B settlements. As global payment networks aggressively fold digital asset infrastructure into traditional corporate banking, the narrative is shifting entirely from retail speculation to institutional utility.

Raj Dhamodharan, executive vice president of blockchain & digital assets at Mastercard, noted that the next phase of stablecoin adoption centers on real-world utility, particularly in settlement, where timing and liquidity are most critical, and that new settlement options are expanding how partners manage liquidity in an always-on digital economy.

For regional fintechs, this always-on framework is becoming a baseline operational standard. PVARA’s statutory compliance updates integrate structured governance frameworks that align with Islamic fintech protocols mature in Saudi Arabia under Vision 2030, offering a shared compliance language for cross-border capital deployment.

However, a critical nuance remains regarding the specific beneficiaries of this legislative perimeter. Zaidi observes that the majority of Karachi-based engineering hubs currently under Gulf due diligence are service-oriented entities, specializing in smart contract architecture and decentralized application development for a global clientele, rather than custodial platforms or trading exchanges.

“Since these teams do not function as custodians or exchanges, the statutory requirements of the Act and PVARA licensing are largely inapplicable to their core operations. A technical squad in Karachi engineering DeFi protocols for an Abu Dhabi-based entity requires no localized virtual asset permit,” Zaidi clarified.

“Consequently, the narrative of a universal compliance shield appears less robust when contrasted with the actual operational mechanics of these software shops.”

Instead, the impact of the Virtual Assets Act is surfacing through the recalibration of investor psychology and valuation multiples. Historically, Gulf-based investment committees applied a standard thirty-percent “haircut” to crypto-adjacent Pakistani firms to account for the structural friction of an unregulated jurisdiction.

By migrating the sector into a formalized regulatory framework, then, the conversation has shifted from legal viability to institutional scalability. For premier development firms with established Western client books, for example, this transition has successfully propelled revenue multiples from historical baselines of 2x toward more aggressive 4x or 5x thresholds.

Beyond fiscal metrics, the socio-professional implications of this formalization are significant. For years, technical teams navigated a precarious gray market, masking incoming foreign exchange as generic software services to satisfy the rigid compliance filters of domestic commercial banks.

“Founders operated in the shadows for a decade, scaling world-class engineering teams while characterizing their output as legacy IT to avoid domestic scrutiny,” Zaidi explained. “The Act has provided the professional legitimacy to engage institutional partners in Riyadh with total transparency, aligning their corporate identity with their technical reality.”

This newfound regulatory clarity is fundamentally altering talent retention strategies. Developers who previously viewed Gulf-based migration as a prerequisite for professional security are increasingly remaining onshore to participate in localized liquidity events. And, while the regional risk premium has not vanished, the alignment of the legal and technical narratives is precisely the stability that international capital is now pricing into the pipeline.

Taxation vs. Talent Retention

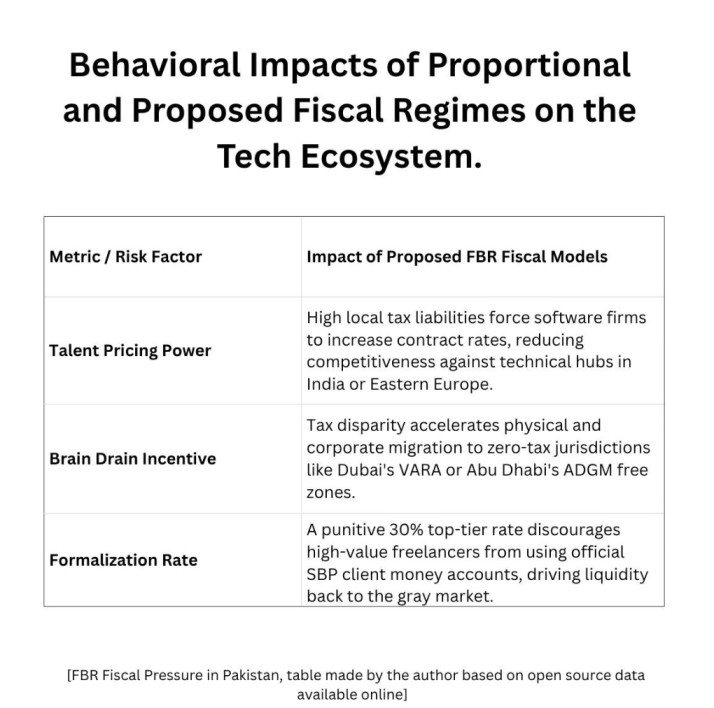

Regardless, this newly minted corridor faces its first real stress test in the upcoming federal budget. To bring digital assets into the formal tax net, the Federal Board of Revenue (FBR) has proposed expanding Section 37 of the Income Tax Ordinance 2001, which would introduce a 10-30% capital gains tax on digital asset transactions, alongside aggressive withholding tax regimes for non-filers.

While intended to capture revenue from a market estimated at $2.5 billion annually, this aggressive fiscal model threatens to disrupt the cost-arbitrage mathematics that drive the corridor.

Meanwhile, the prevailing discourse regarding an imminent fiscal “brain drain” necessitates a pragmatic reassessment. The migration of high-velocity trading liquidity and lucrative Web3 ventures toward zero-tax jurisdictions like Dubai or Ras Al Khaimah is not a prospective threat; it is a matured structural reality established over the previous three years to capitalize on the UAE’s favorable personal tax ecosystem.

Rather than catalyzing a new wave of physical displacement, the FBR’s proposed fiscal tightening will merely compel founders operating across these dual-region corridors to finalize their tax residency. As such, bilateral tax treaties between Pakistan, the UAE, and Saudi Arabia will emerge as the definitive arbiters governing corporate substance and jurisdictional alignment.

The more nuanced macroeconomic peril lies not in the physical departure of technical talent from Karachi, but in the permanent institutionalization of wealth generation offshore. Pakistan faces the structural risk of successfully engineering its onshore plumbing – licensed entities, domestic rupee rails, rigorous compliance frameworks – only to watch tokenized treasuries, intellectual property, and high-margin distributions remain anchored in Dubai.

This bifurcation is driven by domestic fiscal policies that inadvertently penalize local corporate substance. In this architecture, Karachi retains the operational overhead and physical labor force while effectively forfeiting the underlying corporate profit and sovereign wealth accumulation.

The opening of specialized banking rails and clear compliance frameworks has laid down the strongest foundation that the fintech sector has ever seen. Yet, for this pipeline to truly mature into a sustainable economic engine, policymakers must treat it as a high-value export corridor rather than a short-term fiscal target.

In an always-on global digital economy, where technical execution drives sovereign wealth ambition, the final victory will belong to whichever jurisdiction successfully keeps this high-velocity talent pool anchored, compliant, and open for business.

With many thanks to Syed Osama Zaidi (Managing Director at Madarib Capital, Investment Banker; specialized in TMT M&A and digital ecosystem structuring across South Asia and the Gulf) for his invaluable insights.